A Narrative Beyond the Stereotype: Crypto Bros

Why It Matters for Financial Policy and Economic Opportunity

At Open Frontier we are hard at work to build a pro-democracy, pro-worker, and innovation-forward vision for crypto and fintech, understanding who actually leans into it and why is crucial.

Recent data from the Young Men Research Project (YMRP), a broad survey conducted in October 2025, sheds new light on what segments of young adults are investing in crypto, and what this pattern tells us about the financial barriers they face.

Key Takeaways

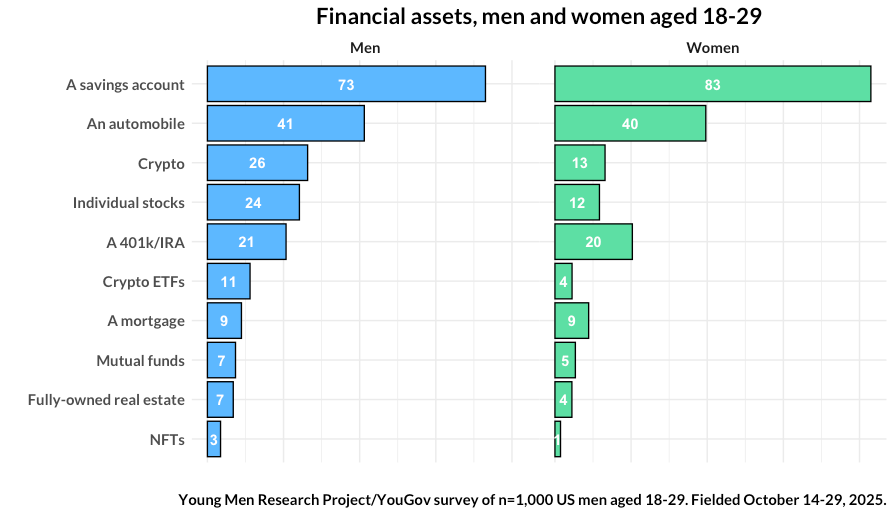

Crypto ownership is real, but not dominant. About 26% of young men aged 18–29 report owning crypto, a slightly higher share than those holding individual stocks (24%) or contributing to a 401(k) / IRA (21%). Most are not exclusively in crypto; instead, crypto tends to be one element of a broader portfolio.

Only a small minority are all in. When we define “all in” as crypto only, without retirement or savings, that group is quite small — roughly 6% of young men in this age range.

Who these all-in investors are matters. They are more commonly found among:

Young men who had traditional financial options but lost access (e.g., lost job with retirement benefits).

Full-time but lower-income workers, and part-time workers without employer-sponsored plans.

Employment and income shape crypto exposure. Those with higher incomes yet no retirement access are disproportionately represented in both general crypto ownership and the small “all in” subset, showing that access to financial vehicles matters more than simple enthusiasm for crypto.

Women participate at lower rates. Although the survey sample of young women was smaller, the patterns show crypto ownership among women is about half that of young men, and virtually no young women meet the “all-in” definition.

A Narrative Beyond the Stereotype

The common stereotype of the crypto investor is the “crypto bro” impulsive, reckless, uninformed, and driven by fear of missing out. But the data suggests a more nuanced story:

Most young people with crypto also participate in standard financial saving and investing vehicles. Crypto isn’t their sole financial strategy, it’s often a part of a larger plan.

For many, crypto isn’t a rejection of traditional savings; it’s a substitute when traditional systems are inaccessible. Where employers offer a 401(k) or IRA, young people take it. Where they don’t, crypto fills the gap.

This helps explain broader trends seen in other polls showing that young men are far more likely to trade or own crypto than women 20–26% vs. much lower shares and that speculative motivations like “fast money” appeal more to them than to other groups.

What This Means for Policy and Employers

If we treat crypto ownership as simply a cultural fad, we risk missing the structural factors behind it. The data suggests:

1. Lack of retirement access drives alternative investing.

Young workers in gig, part-time, or unstable jobs often lack employer-sponsored retirement plans. Without those options, alternative investments — including crypto — become more attractive.

2. Financial literacy alone won’t change behavior.

Messages about “risk” or “long-term investing” ignore the fact that many young people simply don’t have those vehicles available. Policies expanding access to retirement savings (e.g., universal automatic IRAs or incentives for employers to offer plans) could meaningfully shift where young adults allocate capital.

3. Narratives matter.

Framing crypto ownership as “recklessness” or cultural recklessness may push debate toward caricature rather than solutions. Instead, public discussion should focus on why these financial choices are being made and what real barriers exist.

Reframing the Crypto Debate

Only a small share of young people are truly all in on crypto, and those who are often do so not out of folly but out of constrained choice limited access to traditional financial instruments and a desire to grow wealth where they can. Understanding this dynamic is essential for policymakers, employers, educators, and anyone designing systems that shape long-term economic security for the next generation. We need regulation, and clear guide rails to ensure those that are already economically don’t get taken advantage of.